Entrepreneurship

“Acting Like a Startup”

Over the years, I have heard comments like, “We operate like a startup,” “We act like a startup,” and “We are an overnight success that was 10 years in the making.” These statements are often euphemisms for “We are small and not growing as quickly as we would like.”

There are numerous estimates of startups in their first few years. One of the best descriptions I have found is from Failory, but Investopedia and LendingTree have similar but differing take on the statistics and root causes. All three articles linked to are worth reading. The net result is that the outcome of failure is much greater than success, especially over time. So, “acting like a startup” is not necessarily good, even when true. You want to act like a successful startup!

Understanding the data and various causes for success and failure are great inputs to business plans. I have been a principal with successful startups, both early employees and founders. Understanding the data and various causes for success and failure are significant inputs to business plans focused on long-term success. As a Founder, there are a few points that I believe to be key to success:

- You have specific expertise that is in demand and would be valuable to an identifiable number of prospective customers. How would those customers use those skills, and how would they quantify the value? That understanding provides focus on what to sell and to whom.

- A detailed understanding of the market and key players is needed to hone in on a niche to succeed.

- Understand your strengths and weaknesses, then hire the most intelligent and ambitious people who complement your weaknesses and strengths.

- Understand how to reach those potential customers and the messaging you believe will compel them. Then, find a way to test and refine those assumptions as necessary. Marketing and Lead Generation are very important.

- Have a plan for delivering on whatever you sell before you get your first sale. A startup needs to develop its track record of success, beginning with its first sale.

- Cash flow is king. It is far too easy to run out of money while looking at an excellent balance sheet because of receivables. Understand what matters and why.

- Founders need to understand the administrative side of a business – especially the financial, legal (especially contract law), insurance, and taxes. Find experts to validate your approach and fill in knowledge gaps.

- Consistency leads to repeatable success. You standardize, optimize, and automate everything possible. Wasted time and effort become wasted opportunities.

- Finally, there needs to be sufficient cash on hand to fund the time it takes to find and close your first deals, deliver and invoice the work, and then receive your first payments. That could easily be a 3-6 month period.

Those are the foundational items that are reasonably tangible. What is not as concrete but equally as important are:

- Having or developing the ability to spot trends and identify gaps that could become opportunities for your business.

- An agile mindset allows you to pivot your offerings or approach to refine your business model and hone in on that successful niche for your business.

- Foster a sense of innovation within your business. Always look for opportunities to deliver a better product or service, improve the efficiency and effectiveness of your business, and create intellectual property (IP) that adds long-term value.

- Focus on being the best and building a brand that helps differentiate you from your competition.

- Become a Leader, Not a Manager. Create your vision of success, set expectations for each person and team, and help eliminate roadblocks to their success. Trust your team to help you grow and replace members quickly if it becomes clear they are not a good fit.

Steve Jobs once said, “It doesn’t make sense to hire smart people and then tell them what to do; we hire smart people so they can tell us what to do.”

Winning is hard, so focus on the journey. Making your customers’ lives easier and allowing your employees to be creative while doing something they are proud of will lead you to your destination. But when things start going well, don’t sit back and convince yourself you are successful. Instead, continue to focus on ways to improve and grow.

Success means different things to different people, but longevity, growth, profitability, and some form of contributing to the greater good should be dimensions of success for any vision.

Innovations “Iron Triangle”

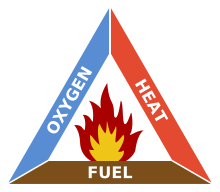

The concept of an Iron Triangle is that along each side of the triangle is one item constrained by the items from the other two sides. In Project Management, this is often referred to as a triple constraint. This identifies the fundamental relationships (such as Time, Cost, and Scope in Project Management) without addressing related aspects such as Risk and Quality. It provides a simple understanding of both requirements and tradeoffs.

Yesterday I spoke with Dave Mosby, an impressive person with an equally impressive background. He related Innovation to Fire, noting that in order to create fire, you need fuel, oxygen, and heat. He added that they must be in the right combination to achieve the desired flame. What a brilliant analogy.

Dave stated that for Corporate Innovation to succeed, you need the proper balance of Innovation, Capital, and Entrepreneurship. I found this enlightening because his description substituted “entrepreneurship” for “culture” in my mental model. While the difference is subtle, I found it to be important.

As noted above, simplified frameworks do not provide a complete understanding. But they help understand and plan around the foundational items required for success. Mapping this to past experiences, I gained a better understanding of things that did not move forward as desired and what I could have done differently to be more effective.

One idea was to create a fault-tolerant database using Red Hat’s JBoss middleware. We had a Services partner willing to create a working prototype, tune it for performance, document the system requirements and configuration, and package it for easy deployment. They wanted $10K to cover their costs.

I did not hold a budget at the time, so I created a purchase request supported by a logical justification. It modeled potential revenue increases for database subscriptions based on the need for a failover installation and growth from potential expanded use cases. This was a slam dunk!

In my mind, this was simple as it was “only $10K,” and I had funded many similar efforts when I had my own company. But that’s the rub. I viewed these efforts as investments in understanding, lessons learned, and growth. Not every investment had a direct payoff, but nearly each had an indirect payoff for my company. It was an entrepreneurial mindset that accepted risk as something required for rewards and success. I now see, many years later, how reframing my proposal as a way to foster innovation and entrepreneurship could have been far more effective.

It is never too late to gain new insights and lessons learned. A slightly different perspective on an important topic provided the understanding that should help position projects for future success. And this flowed from a discussion with an interesting person who has “been there, done that” many times.

Are you Thinking About Starting a Business?

The last post on Starting a Business was popular, so I thought I would share a key lesson learned and then provide links to previous posts that will provide insights as you launch your own business. If you have any questions, just post them as comments; I would happily reply.

The COVID-19 pandemic has created a great deal of uncertainty and opportunity. For many, now is the ideal time to explore their dream of starting a business and jumping into entrepreneurship. That can be exciting, fun, stressful, financially rewarding, and financially challenging, all within the same short period of time.

Being prepared for that roller coaster ride and having the ability and strength to continue pushing forward is important. Something to understand is that “Things don’t happen to you. They are the Direct Result of your own Actions and Inactions.” That may sound harsh, but here is a prime example:

When I was closing my consulting business down, I trusted my Accountant and Payroll company to handle all of the required Federal, Wisconsin, Ohio, and Colorado filings – something they stated they would handle, and I accepted at face value. Both companies had done a great job before, so why would I expect any less this time?

About nine months later, I started receiving letters from Ohio and Colorado about filings due, so I forwarded them to the Accountant and Payroll company. I thought this was “old business” and was being handled, plus I had moved on. It was probably just a timing error, something easy to explain away.

Skipping forward nearly three years, I had been threatened by the IRS and the Revenue Departments from both Ohio and Colorado. I started with a combined total of nearly $500K in assessments. Slowly that dropped to $50K, and then to $10K. I spent countless hours on the phone and writing letters explaining the misunderstanding. It wasn’t until I finally found a helpful person in each department willing to listen and tell me specifically what needed to be done to resolve that situation. My final cost was around $1,000. I was relieved that this fiasco was finally over.

I blamed both the Accountant and Payroll Service for these problems for the longest time. Ultimately I realized that it was my business and, therefore, my responsibility to understand the shutdown process – regardless of who did the work. I would have saved hundreds of hours of my time and several hundred dollars by gaining that understanding initially.

I was not a victim of anything – this situation directly resulted from my own inaction. It did not seem very important at the time, but my understanding of the situation and its importance was incorrect, and I paid the price. Lesson learned. It was my business, so it was still my responsibility to the very end.

Below are the other links. You don’t have to read them all at once, but it would be worth bookmarking them and reading one per day. Every new perspective, idea, and lesson learned could be the thing that helps you achieve your goal a day, week, or month sooner than expected. Every day and every dollar matters, so make the most of both!

- Comments on and a link to an on Curt Culver about Entrepreneurship.

- Comments on and a link to an HBR article about Start-ups and Entrepreneurship.

- Innovation, Intelligent Failure, and Failing Productively.

- Acting Like an Owner – Good Preparation for Becoming an Owner.

- Profitability Through Operational Efficiency.

- What Are You Really Selling?

- Continuous Improvement and a Growth Mindset.

- The Value Created by a Strong Team.

Presentation about Starting a Business and Entrepreneurship

It is interesting how often you see ads for some franchise offering that touts, “Become your own boss.” While that may not be all bad, it is just the tip of the iceberg. The presentation below is intended to provide insight to people considering starting their first company. This was from a one-hour presentation that glosses over many things, such as the need for registrations and insurance, but it could be helpful for a first-timer.

One of the first and most important lessons I learned when I started my consulting company long ago was that paying attention to cash flow was far more important than focusing on my balance sheet. Once you understand a problem, altering what you do to manage it becomes easy. For example, using fixed pricing based on tasks where we received 50% up-front and the remaining 50% upon acceptance of the deliverable smoothed out cash flow, which was a big help.

So, take a look and post any questions that you may have. If one person has a question, many more will likely do as well! Cheers.

Commentary on an HBR article about Start-ups & Entrepreneurship

A friend posted this article on LinkedIn.com. Due to character limitations for comments, I decided to post my response here. Below is a link to the article referenced: https://hbr.org/2019/07/building-a-startup-that-will-last

The article is interesting, but emphasizing “second and third acts” assumes that the start-up will successfully navigate the first act. Even with addressing what the author views as key points this is still a very big assumption. The reasons for Longevity and Success are far more complex and multi-dimensional, but it highlights some of the more important areas of focus.

Long-term success requires several things: The right combination of having a unique goal that has the potential to make a big impact (think “No software” from Salesforce.com); Innovative ideas to achieve that goal; A diverse team to build the product (a mix of visionaries, insightful “translators,” technical experts, designers, planners, adept doers, etc.); Very good sales / business development / marketing to describe a better way of doing things and converting that to new business; and ultimately a management team focused on sustainable and scalable growth.

The point about the need to “Articulate a value framework oriented toward societal impact, not just financial achievement” seems superficial and too tactical.

First, there are unintended consequences to most new technologies. Social Media is a recent example, but Genetic Editing and AI are two areas that are likely to provide more examples over the next decade. Not every societal impact will be positive, and having a negative impact could very well lead to the untimely demise of that company.

Second, the two ideas (societal impact and financial achievement) are not mutually exclusive. When I owned my consulting company, we aimed to fund $1M of medical research to find a cure for Arthritis. We allocated half of our net profits to this goal. Every employee was on board with this because there was a tangible example of why it mattered (my daughter). We invested $500K and helped launch a few careers for some brilliant MD/Ph. Ds and at least one national protocol came out of their research.

Mission and Vision are important to a company, yet many fail to view this as anything more than a marketing effort. Those companies fail to realize that this is as much to motivate and inspire their employees as it is to grab a prospective customer’s attention. These should be inspirational and aspirational, such as the “BHAG” (Big Hairy Audacious Goals) Collins and Porras wrote about 25 years ago.

Regarding Endurance and the assertion that “…the best businesses are intrinsically aligned with the long-term interests of society,” my take is slightly different. The best businesses are always looking for trends and opportunities in an ever-changing global competitive landscape instead of looking to their competitors and trying to ride on their coattails. Companies with a culture of fostering innovation as a way to learn and grow (Amazon and Google are two great examples) are able to find that intersection of “good business” and “positive societal impact.” It is much more complex than a simple one-dimensional outlook.

But it was a good article to help reframe ideas and assumptions around growth.