innovating

Innovations “Iron Triangle”

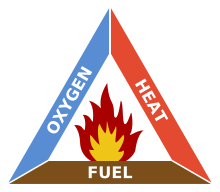

The concept of an Iron Triangle is that along each side of the triangle is one item constrained by the items from the other two sides. In Project Management, this is often referred to as a triple constraint. This identifies the fundamental relationships (such as Time, Cost, and Scope in Project Management) without addressing related aspects such as Risk and Quality. It provides a simple understanding of both requirements and tradeoffs.

Yesterday I spoke with Dave Mosby, an impressive person with an equally impressive background. He related Innovation to Fire, noting that in order to create fire, you need fuel, oxygen, and heat. He added that they must be in the right combination to achieve the desired flame. What a brilliant analogy.

Dave stated that for Corporate Innovation to succeed, you need the proper balance of Innovation, Capital, and Entrepreneurship. I found this enlightening because his description substituted “entrepreneurship” for “culture” in my mental model. While the difference is subtle, I found it to be important.

As noted above, simplified frameworks do not provide a complete understanding. But they help understand and plan around the foundational items required for success. Mapping this to past experiences, I gained a better understanding of things that did not move forward as desired and what I could have done differently to be more effective.

One idea was to create a fault-tolerant database using Red Hat’s JBoss middleware. We had a Services partner willing to create a working prototype, tune it for performance, document the system requirements and configuration, and package it for easy deployment. They wanted $10K to cover their costs.

I did not hold a budget at the time, so I created a purchase request supported by a logical justification. It modeled potential revenue increases for database subscriptions based on the need for a failover installation and growth from potential expanded use cases. This was a slam dunk!

In my mind, this was simple as it was “only $10K,” and I had funded many similar efforts when I had my own company. But that’s the rub. I viewed these efforts as investments in understanding, lessons learned, and growth. Not every investment had a direct payoff, but nearly each had an indirect payoff for my company. It was an entrepreneurial mindset that accepted risk as something required for rewards and success. I now see, many years later, how reframing my proposal as a way to foster innovation and entrepreneurship could have been far more effective.

It is never too late to gain new insights and lessons learned. A slightly different perspective on an important topic provided the understanding that should help position projects for future success. And this flowed from a discussion with an interesting person who has “been there, done that” many times.

Innovation, Optimization, and Business Continuity

Originally posted on LinkedIn.com/in/chipn

Recently I read that the U.S. is experiencing a significant jump in unemployment claims. Much of that is understandable given the recent decline in many businesses, concerns about how long this crisis may last, and the need to protect ongoing viability by business owners and executives. But, in the near future, business activity will resume, and it will be very important that businesses maintain a business pipeline and retain qualified staff to deliver their products and services.

Now could be the ideal time to challenge your team to focus on improving your business. Look at business processes and identify:

- What works well today? Are you able to identify what makes it work so well? Simplicity, automation, and lack of friction are typical attributes of effective and efficient systems and processes that positively impact any business.

- What could be improved and why? Specific examples and real data will help quantify the impact and support prioritizing follow-up activities.

- What is missing today?

- Good ideas have likely been raised in the past, so why not revisit them?

- What are competitors or businesses in other segments doing that could be helpful?

- Brainstorm and consider something completely new that could help your business.

- Start a list, describe the needs and benefits, provide specific examples, and then estimate each idea’s potential impact and time to value.

- Take the ideas with the greatest promise and estimate the cost, people/skills needed, and other dependencies to see how they stack up.

Something else to consider is the creation or updating of Business Continuity Plans. Now is a perfect time – while everything is fresh in the minds of your team. Not only will this help in the future, but there could also be several useful ideas for the coming weeks.

For example, do you have sufficient documentation for someone who is not an expert in your business to take over with a relatively small ramp-up time? How will you maintain quality and control of those processes? Are your plans stored in a repository that is accessible yet secure outside of your organization? Do you have the processes and tools to collect documentation and feedback on things that did not work as documented or could be improved? Are your Risk Management plans and mitigation procedures up-to-date and adequate?

Investing in your business during this slowdown could have many benefits, including maintaining employee morale, enhancing employee and customer loyalty, retaining employees and their expertise and skills, and increasing sustainability and long-term growth potential.

Are you Visionary or Insightful?

Having great ideas that are not understood or validated is pointless, just as being great at “filling in the gaps” to do amazing things does not accomplish much if what you are building achieves little toward your needs and goals. This post is about Dreaming Big and turning those dreams into actionable plans.

Let me preface this post by stating that both are important and complementary roles. But, if you don’t recognize the difference between the two, it becomes much more challenging to execute and realize value/gain a competitive advantage.

The Visionary has great ideas but doesn’t always create plans or follow through on developing the idea. There are many reasons why this happens (distractions, new interests, frustration, lack of time), so it is good to be aware of that, as this type of person can benefit by being paired with people willing and able to understand a new idea or approach, and then take the next steps to flesh out a high-level plan to present that idea and potential benefits to key stakeholders. People may view them as aloof or unfocused.

The Insightful sees the potential in an idea, helps others understand the benefits and gain their support, and often creates and executes a plan to prototype and validate the idea – killing it off early if the anticipated goals are unachievable. They document, learn from these experiences, and become more and more proficient with validating the idea or approach and quantifying the potential benefits. They are usually very pragmatic.

Neither of these types of people is affected by loss aversion bias.

I find it amazing how frequently you hear someone referred to as being Visionary, only to see that the person in question could eliminate some of the noise and “see further down the road” than most people. While this skill is valuable, it is more akin to analytics and science than art. Insight usually comes from focus, understanding, intelligence, and being open-minded. Those qualities matter in both business and personal settings.

On the other hand, someone truly visionary looks beyond what is already illuminated and can, therefore, be detected or analyzed. It’s like a game of chess where the visionary person is thinking six or seven moves ahead. They are connecting the dots for the various future possibilities while their competitor is still thinking about their next move.

Interestingly, this can be a very frustrating situation for everyone.

- The Visionary with an excellent idea may become frustrated because they feel an unmet need to be understood.

- The people around that visionary person become frustrated, wondering why that person isn’t able to focus on what is important or why they fail to see/understand the big picture.

- Others view the visionary ideas and suggestions as tangential or irrelevant. It is only over time that the others understand what the visionary person was trying to show them – often after a competitor has started executing a similar idea.

- The Insightful wanting to make a difference can feel constrained in static environments, offering little opportunity for change and improvement.

Both Insightful and Visionary people feel that they are being strategic. Both believe they are doing the right thing. Both have similar goals. What’s truly ironic is they may view each other as the competition rather than seeing the potential of collaborating.

A strong management team can positively impact creativity by fostering a culture of innovation and placing these people together to work towards a common goal. Providing little time and resources to explore an idea can lead to remarkable outcomes. When I had my consulting company, I sometimes joked, “What would Google do?” to describe that amazing things were possible and waiting to be done.

The insightful person may see a payback on their ideas sooner than the visionary person, and that is due to their focus on what is already in front of them. It may be a year or more before what the visionary person has described shifts to the mainstream and into the realm of insight – hopefully before it reaches the realm of common sense (or worse yet, is entirely passed by).

I recommend that people create a system to gather ideas, along with a description of what the purpose, goals, and advantages of those ideas are. Foster creative behavior by rewarding people for participation regardless of what becomes of the idea. Review those ideas regularly and document your commentary. You will find good ideas with luck – some insightful and possibly even visionary.

Look for commonalities and trends to identify the people who can cut through the noise or see beyond the periphery and the areas having the greatest innovation potential. This approach will help drive your business to the next level.

You never know where the next good idea will come from. Efforts like these provide growth opportunities for people, products, and profits.

Failing Productively

As an entrepreneur, you will typically get advice like, “Fail fast and fail often.” I always found this somewhat amusing, similar to the saying, “It takes money to make money” (a lot of bad investments are made using that philosophy). Living this yourself is an amazing experience – especially when things turn out well. But as I have written about before, you learn as much from the good experiences as you do from the bad ones.

Innovating is tough. You need people who always think of different and better ways of doing things or question why something has to be done or made a certain way. It means shifting away from the “how” and “why” and focusing on the “what” (outcomes). It takes confidence to ask questions that many would view as stupid (“Why would you do that, it’s always been done this way.”) But, when you have the right mix of people and culture, amazing things can and do happen, and it feels great.

Innovating also takes a willingness to lose time and money, hoping to win something big enough later to make it all worthwhile. This is where many companies fall short because they lack the patience, budget, or appetite to fail. I personally believe that this is the reason why innovation often flows from small companies and small teams. For them, the prospect of doing something cool or making a big impact is motivation enough to try something, and the barriers to getting started are often much lower.

It takes a lot of discipline to follow a plan when a project appears to be failing, but it takes even more discipline to kill a project that has demonstrated real potential but isn’t meeting expectations. That was one of my first and probably most important lessons learned in this area. Let me explain…

In 2000 we looked at franchising our “Consulting System” – processes, procedures, tools, metrics, etc., developed and proven in my business. We believed this approach could help average consultants deliver above-average work products in less time. The idea seemed to have real potential.

Finding an attorney who would even consider this idea took a lot of work. Most believed it would be impossible to proceduralize a somewhat ambiguous task like solving a business or technical problem. We finally found an attorney who, after a 2-hour no-cost interview, agreed to work with us. When asked about his approach, he replied, “I did not want to waste my [his] time or our money on a fool’s errand.”

We estimated it would take 12 months and cost approximately $100,000 to fully develop our consulting system. We met with potential prospects to validate the idea (it would have been illegal to pre-sell the system) and then got to work. Twelve months turned into 18, and the original $100K budget increased nearly 50%. All indications were positive, and we felt very good about the success and business potential of this effort.

Then, the terror attacks occurred on Sept. 11th and businesses everywhere saw a decline. In early 2002 we reevaluated the project and felt that it could be completed within the next 6-8 months and would cost another $50K+.

After a long and emotional debate, we decided to kill the project – not because we felt it would not work, but because there was less of a target market, and now the payback period (time to value) would double or triple. This was one of the most difficult business decisions that I ever made.

A big lesson learned from this experience was that our approach needed to be more analytical.

- From that point forward, we created a budget for “time off” (we bought our own time, as opposed to waiting for bench time) and other project-related items.

- We developed a simple system for collecting and tracking ideas and feedback. When an idea felt right, we would take the next steps and create a plan with a defined budget, milestones, and timeline. If the project failed to meet any defined objectives, it would be killed – No questions asked.

- We documented what we did, why we decided to do it, our goals, and expected outcomes and timelines. Regardless of success or failure, we would conduct postmortem reviews to learn and document as much as possible from every effort and investment.

We still had failures, but with each one, we took less time and spent less money. More importantly, we learned how to do this better, which helped us realize several successes. It provided both the structure and the freedom to create some amazing things. Since failing was an acceptable outcome, it was never feared.

This approach was more than just “failing fast and failing often”; it was “intelligent failure,” which served us well for nearly a decade.