selling

Doing it like Mike

My son is playing basketball this year (previously, he played football and soccer), and recently we went shopping for new shoes. Each store had pictures of Michael Jordan. I used to love watching MJ play with the Chicago Bulls. He was the epitome of skill and professionalism. To this day, he inspires me.

Some people are naturally talented but must still work hard to achieve their full potential. Hard work is an important aspect of being the best at anything, but it takes more than that. It takes doing things in a manner that allows you to continuously improve, as well as a positive mindset and a commitment to success. Once people reach that high-performance level, their jobs look easy, and they may even appear to be a “natural” – just like Mike. But that is just the tip of the iceberg.

Most of my career changes have been unplanned. Opportunities presented themselves, the job seemed interesting, and before I knew it, I was fully immersed in something related but different. The potential reward outweighed the real risk.

Many of these things have not come naturally to me. Each time I focused on understanding the requirements for doing the job well, then looked for examples of exceptional performance, and finally created a systematic approach that allowed me to measure performance and identify areas of improvement on an ongoing basis. From then on it was analyzing my results, thinking daily about even the smallest improvements, and then trying to do even better the next day.

Good enough was never good enough. Introspection can be challenging, so one thing that I have done is to take time to celebrate wins and intentionally focus on remembering how that feels. Those memories can be motivational in times of stress or frustration and help you get back on track quickly.

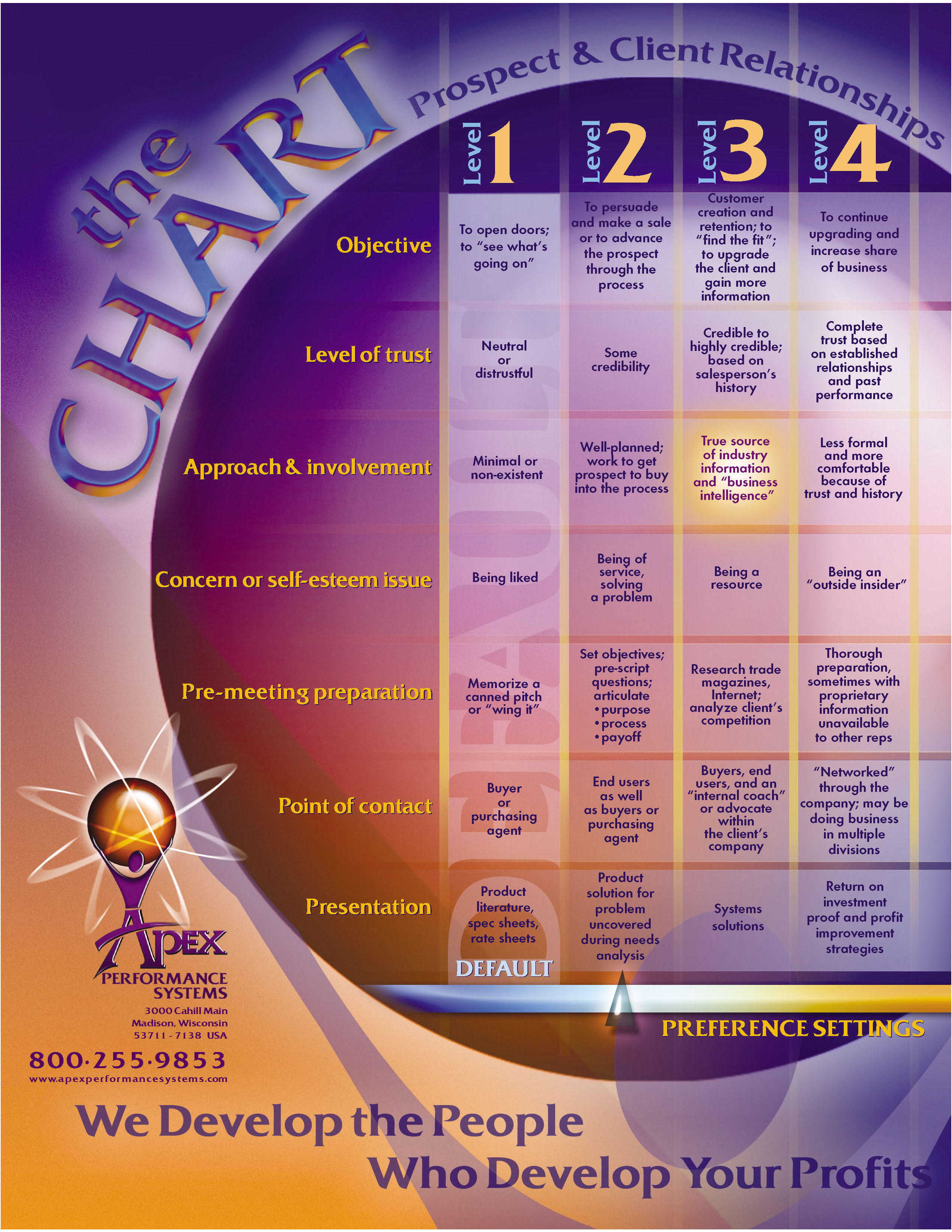

Sales have been a large part of my consulting management jobs since the mid-1990s, but it wasn’t until I owned my own company that this became a true priority. I ran across a good book, The Accidental Salesperson, by Chris Lytle. Back then, Chris Lytle had “MAX Training,” and a large part of their focus was increasing your “level” with regard to Prospect and Client relationships. The training was good and was complementary to systems like Miller Heiman.

What each of these systems do is help you prepare, plan, and execute to the best of your ability. And just like basketball, it takes practice to master. With mastery comes success and the illusion that something is easy (or you are lucky). The Seneca quote, “Luck is what happens when preparation meets opportunity,” is so true.

Regardless of the system used, what is most important is that you are trying to be the best at is to look at both positive and negative examples to see what you can learn from them. There are lessons to be learned everywhere! Understanding what makes it good or bad helps you improve as part of an ongoing improvement process.

Incorporating new tools and techniques into what has already been proven to work will help you improve your game. Returning to the sports analogy, this could be part of what made Michael Jordon so good. He would see something interesting, improve it, and then make it his own.

For example, I get many horrible sales calls and emails. The people have obviously not done any preparation, do not know anything about me or the company I work for, and often remind me of why I stopped listening to them by referring to the number of times they have tried contacting me. On the other hand, some talented sales professionals have done their homework, understand their products and the competition, and understand why what they are selling should matter to me – and can articulate that quickly and confidently. I will speak with them and occasionally buy from them. And in either case I provide my team with real-life examples of good and bad sales techniques.

So, think of the best example of whatever it is you do, and see what you can do to become more like them. This isn’t about imitation but rather about uncovering the secrets of their success and learning from them. And have some fun doing it!

Acting like an Owner – Does it matter?

One of the biggest changes to my professional perspective on business came when I started my own consulting business. Prior to that, I had worked as an employee for midsize to large companies for ten years and then as one of the first hires at a start-up technology company. I felt that doing hands-on work, managing, selling, and helping establish a start-up (where I did not have an equity stake) provided everything needed to start my own business.

Well, guess what? I was only partially correct. I was prepared for the activities of running the business but really was not prepared for the responsibility of running a business. While this seems like it should be obvious, I’ve seen many business owners whose primary focus is on growth/upside activities and not the day-to-day. That type of optimism is important for entrepreneurs – without it, they would not bother putting so much at risk.

People tend to adopt a different perspective when making decisions once they realize that every action and decision can impact the money moving into and out of their own wallets.

Even in a large business, you can usually spot the people who have taken these risks and run their own business. I was responsible for a Global Business Unit with $60+ million in annual sales and ran it like a “business within a business.” Having P&L responsibilities meant the decisions I made mattered to my success and the success of my business unit.

It’s more than just striking out on your own as a contractor or sole proprietor. I’m talking about the people who have had employees, invested in capital equipment and went all-in. These are the people thinking about the big picture and the future.

What do these people do differently than those without this type of experience?

One of the biggest things is they view business as “good business” and “bad business.” Not all business is good business, and not all customers are good customers. There needs to be a fair commercial exchange where both sides receive value, mutual respect, and open communication. You know this works when your customers treat you like a true partner (a real trusted advisor) instead of just a vendor, or at least do not try to take advantage of you (and vice-versa).

A business is in business to make money, so if your work is not profitable, you should not do it. And, if you are not delivering value to an organization, it is very likely that you would be better off spending your time elsewhere – building your reputation and reference base within an organization that was a better fit. While that may not be true for all business endeavors (think how long it took Amazon to become profitable and where they are now), it generally is true for employees at all levels.

“Bad” salespeople (who may very well regularly exceed their quotas) only care about the sale and their commission – not the fit, the customer’s satisfaction, or the effort required to support that customer. Selling products and services people don’t need, charging too little or too much, and making promises they know will not be met are typical signs of a person who does not think like an owner. Their focus is on the short-term and not on growing accounts. As an aside, their compensation plans generally only reward net new business and first-time sales, not ongoing customer satisfaction, so these actions may not be completely their fault.

How you view and treat employees is another big difference. Unfortunately, even business owners do not always get this right. I believe that employees are either viewed as Assets (to be managed for growth and long-term value) or Commodities (to be used up and replaced as needed – usually treated as fungible, as if they are easily replaceable). Your business is usually only as good as your employees, so treating them well and with respect creates loyalty and results in higher customer satisfaction.

Successful business owners usually look for the best person out there, not just the most affordable person who is “good enough” to do the job. On the flip side, you quickly need to weed out the people who are not a good fit. Making good decisions quickly and decisively is often a hallmark of a successful business owner. The saying about hiring slowly and firing quickly makes even more sense when you are running a lean operation that requires every person to contribute to the success of the company.

Successful business owners are generally more innovative. They are willing to experiment and take risks. They reward that behavior. They understand the need to find a niche where they can win and provide goods and/or services tailored to those specific needs.

Sometimes, this means specialization and customization, and sometimes, it means personalized attention and better support. Regardless of what is different, these people observe the small details, understand their target market, and are good at defining a message articulating those differences. These are the people who seem to be able to see around corners and anticipate both problems and opportunities. They do this out of necessity.

Former business owners are usually more conscientious about money, taking a “my money” perspective on sales and expenses. Every dollar in the business provides safety and opportunity for growth. These usually are not the people who routinely spend hundreds or thousands of dollars on business meals or who take unnecessary or questionable trips to nice places. Money saved on unnecessary expenses can be invested in new products, features, or marketing for the benefit of an organization.

While these are common traits of successful business owners, you can develop them even if you have never owned a business.

When selling, are you focused on delivering value, developing a positive reputation within that organization and with your customers, and profiting from long-term relationships? When delivering services, is your focus on delivering what has been contracted – and doing so on time and within budget? Are your projects used as examples of how things should be done within other organizations? Are you spending money on the right things – not wasteful or extravagant things?

These are things employees at all levels can do. They will make a difference and help you stand out. That opens the door to career growth and change. And it may get you thinking about starting the business you have always dreamed of. Awareness and understanding are the first steps towards change and improvement.

There’s a story in there – I just know it…

I was reading an article from Nancy Duarte about Strengthening Culture with Storytelling, and it made me think about how important a skill storytelling can be in business and how it can be far more effective than just presenting facts and data. These are just a few examples. You probably have many of your own.

One of the best salespeople I’ve ever known wasn’t a salesperson at all. It is Jon Vice, former CEO of the Children’s Hospital of Wisconsin. Jon is very personable and has the ability to make each person feel like they are the most important person in the room (quite a skill in itself). Jon would talk to a room of people and tell a story. Mid-story, you were hooked. You completely bought what he was selling, often without knowing what the “ask” was. It was an amazing thing to experience.

Years ago, when my company was funding medical research projects, my oldest daughter (then only four years old) and I watched a presentation on the mid-term findings of one of the projects. The MD/Ph.D. giving the presentation was impressive, but what he showed was slide after slide of data. After 10-15 minutes, my daughter held her Curious George stuffed animal up in front of her (where the shadow would be seen on the screen) and proclaimed, “Boring!”

Six months later, that same person gave his wrap-up presentation. It was short and told an interesting story that explained why these findings were important, laying the groundwork for a follow-on project. A few years later he commented that his initial presentation became a valuable lesson. That was when he realized the story the data told was far more compelling than just the data itself.

A few years ago, the company I work for introduced a high-performance analytics database. We touted that our product was 100 times faster than other products, which happened to be a similar message used by a handful of competitors. In my region, we created a “Why Fast Matters” webinar series and told the stories of our early Proof of Value efforts. This helped my team make the first few sales of this new product and change the approach the rest of the company used to position this product. People understood our value proposition because these success stories made the facts tangible.

I tell my teams to weave the thread of our value proposition into the fabric of a prospect’s story. This makes us part of the story and makes this new story their own (as opposed to our story). This simple approach has been very effective.

What if you not selling anything? Your data tells a story – even more so with big data. Whether you are analyzing data from a single source (such as audit or log data) or correlating data from multiple sources, the data has a story to tell. Whether patterns, trends, or correlated events – the story is there. And once you find it, there is so much you can do to build it out.

Whether you are selling, managing, teaching, coaching, analyzing, or just hanging out with friends or colleagues, being able to entertain with a story is a valuable skill. It is also a great way to make many things more interesting and memorable in business. So, give it a try.

What’s the prize if I win?

In consulting and in business, there is a tendency to believe that if you show someone how to find that proverbial “pot of gold at the end of the rainbow,” they will be motivated to do so. Seasoned professionals will tend to ask, “What problem are you trying to solve?” to understand whether there is a real opportunity. If you cannot quickly, clearly, and concisely articulate the problem, and why this helps solve it, it is often game over then and there (N.B. It pays to be prepared). But, having the right answer is not a guarantee of moving forward.

Unfortunately, sometimes a mere pot of gold just isn’t enough to motivate. Sometimes it takes something different, and usually something personal. It’s more, “What’s in this for me?” No, I am not talking about bribes, kickbacks, or anything illegal or unethical. This is about determining what is really important to the decision maker and in what priority, and then demonstrating that the proposed solution will bring them closer to achieving their personal goals. What’s in it for them?

Case in point. Several years ago I was trying to sell a packaged Business Intelligence (BI) system developed on our database platform to customers most likely to have a need. Qualification performed – check. Interested – check. Proof of value – check. Quick ROI – check. Close the deal – not so fast…

This application was a set of dashboards with 150-200 predefined KPIs (key performance indicators). The premise was that you could quickly tailor and deploy the new BI system with little risk (finding and validating the data needed was available to support the KPI was the biggest risk, but one that could be identified up-front) and about half the cost of what a similar typical implementation would cost. Who wouldn’t want one?

I spent several days onsite with the prospect, identified areas of concern and opportunity, and used their data to quantify the potential benefit. Before the end of the week, I was able to show the potential to get an 8x ROI in the first year. Remember, this was estimated using their data, not figures I just created. Being somewhat conservative, I suggested that even half that amount would be a big success. Look – we found the pot of gold!

Despite this, the deal never closed. This company had a lot of money, and this CIO had a huge budget. Saving $500K+ would be nice but was not essential. What I learned later was that this person was pushing forward an initiative of his own that was highly visible. This new system had the potential to become a distraction, and he did not need that. Had I made this determination sooner, I could have easily repositioned it to align with his agenda.

For example, the focus of the system could have shifted from financial savings to project and risk management for his higher priority initiative. The KPIs could be on earned value, scheduling, and deliverables. This probably would have sold as it would have been far more appealing to this CIO and supported what was important to him (i.e., his prize if he wins). The additional financial savings initially identified would be the icing on the cake, to be applied later.

There were several lessons learned from this effort. In this instance, I focused on my personal pot of gold (based on logic and common sense) rather than on my customer’s priorities and prize for winning. That mistake cost me this deal, but it is one I have not made since – helping me win many other deals.

- ← Previous

- 1

- 2